Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

"the strat" için komut dosyalarını ara

Long/Short/Exit/Risk management Strategy # LongShortExit Strategy Documentation

## Overview

The LongShortExit strategy is a versatile trading system for TradingView that provides complete control over entry, exit, and risk management parameters. It features a sophisticated framework for managing long and short positions with customizable profit targets, stop-loss mechanisms, partial profit-taking, and trailing stops. The strategy can be enhanced with continuous position signals for visual feedback on the current trading state.

## Key Features

### General Settings

- **Trading Direction**: Choose to trade long positions only, short positions only, or both.

- **Max Trades Per Day**: Limit the number of trades per day to prevent overtrading.

- **Bars Between Trades**: Enforce a minimum number of bars between consecutive trades.

### Session Management

- **Session Control**: Restrict trading to specific times of the day.

- **Time Zone**: Specify the time zone for session calculations.

- **Expiration**: Optionally set a date when the strategy should stop executing.

### Contract Settings

- **Contract Type**: Select from common futures contracts (MNQ, MES, NQ, ES) or custom values.

- **Point Value**: Define the dollar value per point movement.

- **Tick Size**: Set the minimum price movement for accurate calculations.

### Visual Signals

- **Continuous Position Signals**: Implement 0 to 1 visual signals to track position states.

- **Signal Plotting**: Customize color and appearance of position signals.

- **Clear Visual Feedback**: Instantly see when entry conditions are triggered.

### Risk Management

#### Stop Loss and Take Profit

- **Risk Type**: Choose between percentage-based, ATR-based, or points-based risk management.

- **Percentage Mode**: Set SL/TP as a percentage of entry price.

- **ATR Mode**: Set SL/TP as a multiple of the Average True Range.

- **Points Mode**: Set SL/TP as a fixed number of points from entry.

#### Advanced Exit Features

- **Break-Even**: Automatically move stop-loss to break-even after reaching specified profit threshold.

- **Trailing Stop**: Implement a trailing stop-loss that follows price movement at a defined distance.

- **Partial Profit Taking**: Take partial profits at predetermined price levels:

- Set first partial exit point and percentage of position to close

- Set second partial exit point and percentage of position to close

- **Time-Based Exit**: Automatically exit a position after a specified number of bars.

#### Win/Loss Streak Management

- **Streak Cutoff**: Automatically pause trading after a series of consecutive wins or losses.

- **Daily Reset**: Option to reset streak counters at the start of each day.

### Entry Conditions

- **Source and Value**: Define the exact price source and value that triggers entries.

- **Equals Condition**: Entry signals occur when the source exactly matches the specified value.

### Performance Analytics

- **Real-Time Stats**: Track important performance metrics like win rate, P&L, and largest wins/losses.

- **Visual Feedback**: On-chart markers for entries, exits, and important events.

### External Integration

- **Webhook Support**: Compatible with TradingView's webhook alerts for automated trading.

- **Cross-Platform**: Connect to external trading systems and notification platforms.

- **Custom Order Execution**: Implement advanced order flows through external services.

## How to Use

### Setup Instructions

1. Add the script to your TradingView chart.

2. Configure the general settings based on your trading preferences.

3. Set session trading hours if you only want to trade specific times.

4. Select your contract specifications or customize for your instrument.

5. Configure risk parameters:

- Choose your preferred risk management approach

- Set appropriate stop-loss and take-profit levels

- Enable advanced features like break-even, trailing stops, or partial profit taking as needed

6. Define entry conditions:

- Select the price source (such as close, open, high, or an indicator)

- Set the specific value that should trigger entries

### Entry Condition Examples

- **Example 1**: To enter when price closes exactly at a whole number:

- Long Source: close

- Long Value: 4200 (for instance, to enter when price closes exactly at 4200)

- **Example 2**: To enter when an indicator reaches a specific value:

- Long Source: ta.rsi(close, 14)

- Long Value: 30 (triggers when RSI equals exactly 30)

### Best Practices

1. **Always backtest thoroughly** before using in live trading.

2. **Start with conservative risk settings**:

- Small position sizes

- Reasonable stop-loss distances

- Limited trades per day

3. **Monitor and adjust**:

- Use the performance table to track results

- Adjust parameters based on how the strategy performs

4. **Consider market volatility**:

- Use ATR-based stops during volatile periods

- Use fixed points during stable markets

## Continuous Position Signals Implementation

The LongShortExit strategy can be enhanced with continuous position signals to provide visual feedback about the current position state. These signals can help you track when the strategy is in a long or short position.

### Adding Continuous Position Signals

Add the following code to implement continuous position signals (0 to 1):

```pine

// Continuous position signals (0 to 1)

var float longSignal = 0.0

var float shortSignal = 0.0

// Update position signals based on your indicator's conditions

longSignal := longCondition ? 1.0 : 0.0

shortSignal := shortCondition ? 1.0 : 0.0

// Plot continuous signals

plot(longSignal, title="Long Signal", color=#00FF00, linewidth=2, transp=0, style=plot.style_line)

plot(shortSignal, title="Short Signal", color=#FF0000, linewidth=2, transp=0, style=plot.style_line)

```

### Benefits of Continuous Position Signals

- Provides clear visual feedback of current position state (long/short)

- Signal values stay consistent (0 or 1) until condition changes

- Can be used for additional calculations or alert conditions

- Makes it easier to track when entry conditions are triggered

### Using with Custom Indicators

You can adapt the continuous position signals to work with any custom indicator by replacing the condition with your indicator's logic:

```pine

// Example with moving average crossover

longSignal := fastMA > slowMA ? 1.0 : 0.0

shortSignal := fastMA < slowMA ? 1.0 : 0.0

```

## Webhook Integration

The LongShortExit strategy is fully compatible with TradingView's webhook alerts, allowing you to connect your strategy to external trading platforms, brokers, or custom applications for automated trading execution.

### Setting Up Webhooks

1. Create an alert on your chart with the LongShortExit strategy

2. Enable the "Webhook URL" option in the alert dialog

3. Enter your webhook endpoint URL (from your broker or custom trading system)

4. Customize the alert message with relevant information using TradingView variables

### Webhook Message Format Example

```json

{

"strategy": "LongShortExit",

"action": "{{strategy.order.action}}",

"price": "{{strategy.order.price}}",

"quantity": "{{strategy.position_size}}",

"time": "{{time}}",

"ticker": "{{ticker}}",

"position_size": "{{strategy.position_size}}",

"position_value": "{{strategy.position_value}}",

"order_id": "{{strategy.order.id}}",

"order_comment": "{{strategy.order.comment}}"

}

```

### TradingView Alert Condition Examples

For effective webhook automation, set up these alert conditions:

#### Entry Alert

```

{{strategy.position_size}} != {{strategy.position_size}}

```

#### Exit Alert

```

{{strategy.position_size}} < {{strategy.position_size}} or {{strategy.position_size}} > {{strategy.position_size}}

```

#### Partial Take Profit Alert

```

strategy.order.comment contains "Partial TP"

```

### Benefits of Webhook Integration

- **Automated Trading**: Execute trades automatically through supported brokers

- **Cross-Platform**: Connect to custom trading bots and applications

- **Real-Time Notifications**: Receive trade signals on external platforms

- **Data Collection**: Log trade data for further analysis

- **Custom Order Management**: Implement advanced order types not available in TradingView

### Compatible External Applications

- Trading bots and algorithmic trading software

- Custom order execution systems

- Discord, Telegram, or Slack notification systems

- Trade journaling applications

- Risk management platforms

### Implementation Recommendations

- Test webhook delivery using a free service like webhook.site before connecting to your actual trading system

- Include authentication tokens or API keys in your webhook URL or payload when required by your external service

- Consider implementing confirmation mechanisms to verify trade execution

- Log all webhook activities for troubleshooting and performance tracking

## Strategy Customization Tips

### For Scalping

- Set smaller profit targets (1-3 points)

- Use tighter stop-losses

- Enable break-even feature after small profit

- Set higher max trades per day

### For Day Trading

- Use moderate profit targets

- Implement partial profit taking

- Enable trailing stops

- Set reasonable session trading hours

### For Swing Trading

- Use longer-term charts

- Set wider stops (ATR-based often works well)

- Use higher profit targets

- Disable daily streak reset

## Common Troubleshooting

### Low Win Rate

- Consider widening stop-losses

- Verify that entry conditions aren't triggering too frequently

- Check if the equals condition is too restrictive; consider small tolerances

### Missing Obvious Trades

- The equals condition is extremely precise. Price must exactly match the specified value.

- Consider using floating-point precision for more reliable triggers

### Frequent Stop-Outs

- Try ATR-based stops instead of fixed points

- Increase the stop-loss distance

- Enable break-even feature to protect profits

## Important Notes

- The exact equals condition is strict and may result in fewer trade signals compared to other conditions.

- For instruments with decimal prices, exact equality might be rare. Consider the precision of your value.

- Break-even and trailing stop calculations are based on points, not percentage.

- Partial take-profit levels are defined in points distance from entry.

- The continuous position signals (0 to 1) provide valuable visual feedback but don't affect the strategy's trading logic directly.

- When implementing continuous signals, ensure they're aligned with the actual entry conditions used by the strategy.

---

*This strategy is for educational and informational purposes only. Always test thoroughly before using with real funds.*

nineLivesUtilLibLibrary "nineLivesUtilLib"

isDateInRange(currentTime, useTimeFilter, startDate, endDate)

Checks if the current time is within the specified date range.

Parameters:

currentTime (int) : The current bar's time (time).

useTimeFilter (bool) : Bool 📅: Enable the date range filter.

startDate (int) : Timestamp 📅: The start date for the filter.

endDate (int) : Timestamp 📅: The end date for the filter.

Returns: True if the current time is within the range or filtering is disabled, false otherwise.

@example

inDateRange = nineLivesUtilLib.isDateInRange(time, useTimeFilter, startDate, endDate)

if inDateRange

// Execute trading logic

checkVolumeCondition(currentVolume, useVolumeFilter, volumeThresholdMultiplier, volumeLength)

Checks if the current volume meets the threshold condition.

Parameters:

currentVolume (float) : The current bar's volume (volume).

useVolumeFilter (bool) : Bool 📊: Enable the volume filter.

volumeThresholdMultiplier (float) : Float 📊: Volume threshold relative to average (e.g., 1.5 for 1.5x average).

volumeLength (int) : Int 📊: Lookback length for the volume average.

Returns: True if the volume condition is met or filtering is disabled, false otherwise.

@example

volumeOk = nineLivesUtilLib.checkVolumeCondition(volume, useVolumeFilter, volumeThreshold, volumeLength)

if volumeOk

// Proceed with trading logic

checkMultiTimeframeCondition(currentClose, currentOpen, htfClose, htfOpen, useMultiTimeframe, alignment)

Checks alignment with higher timeframe direction.

Parameters:

currentClose (float) : Float: The current bar's closing price (close).

currentOpen (float) : Float: The current bar's opening price (open).

htfClose (float) : Float: The closing price from the higher timeframe (must be fetched by the calling script using request.security).

htfOpen (float) : Float: The opening price from the higher timeframe (must be fetched by the calling script using request.security).

useMultiTimeframe (bool) : Bool ⏱️: Enable multi-timeframe analysis.

alignment (string) : String ⏱️: Desired alignment ("same", "opposite", "any").

Returns: True if the timeframe alignment condition is met or analysis is disabled, false otherwise.

@example

// In the calling script:

= request.security(syminfo.tickerid, higherTimeframe, )

tfOk = nineLivesUtilLib.checkMultiTimeframeCondition(close, open, htfClose, htfOpen, useMultiTimeframe, tfAlignment)

if tfOk

// Proceed with trading logic

checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

Detects the market regime (trending or ranging) and checks if trading is allowed.

Parameters:

useMarketRegime (bool) : Bool 🔍: Enable market regime detection.

regimeIndicator (string) : String 🔍: Indicator to use ("ADX" or "Volatility").

regimeThreshold (int) : Int 🔍: Threshold for trend strength/volatility.

regimeLength (simple int) : Int 🔍: Lookback length for the indicator.

regimeMode (string) : String 🔍: Trading mode based on regime ("trend_only", "range_only", "adaptive").

Returns: A tuple containing:

: conditionMet (bool) - True if trading is allowed based on the regime mode and detection, false otherwise.

: inTrendingRegime (bool) - True if the current regime is trending based on the indicator and threshold.

@example

= nineLivesUtilLib.checkMarketRegime(useMarketRegime, regimeIndicator, regimeThreshold, regimeLength, regimeMode)

if regimeOk

// Proceed with trading logic

applyCooldown(buySignal, sellSignal, cooldownBars)

Applies a cooldown period after a signal.

Parameters:

buySignal (bool) : Bool: Buy signal (potentially after primary entry logic).

sellSignal (bool) : Bool: Sell signal (potentially after primary entry logic).

cooldownBars (int) : Int ⏳: The number of bars to wait after a signal before allowing another.

Returns: A tuple containing:

: cooldownFilteredBuy (bool) - Buy signal after cooldown filter.

: cooldownFilteredSell (bool) - Sell signal after cooldown filter.

@example

= nineLivesUtilLib.applyCooldown(rawBuySignal, rawSellSignal, iCool)

applyAllFilters(rawBuy, rawSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, drawdownOk, cooldownOkBuy, cooldownOkSell)

Applies all filtering conditions to the buy and sell signals.

Parameters:

rawBuy (bool) : Bool: The initial buy signal candidate (from primary entry logic, e.g., after cooldown).

rawSell (bool) : Bool: The initial sell signal candidate (from primary entry logic, e.g., after cooldown).

inDateRange (bool) : Bool 📅: Result from isDateInRange.

tradeDirection (string) : String 🔄: Overall trade direction preference ("longs_only", "shorts_only", "both").

volumeOk (bool) : Bool 📊: Result from checkVolumeCondition.

tfOk (bool) : Bool ⏱️: Result from checkMultiTimeframeCondition.

regimeOk (bool) : Bool 🔍: Result from checkMarketRegime.

drawdownOk (bool) : Bool 📉: Result from checkDrawdownExceeded (or equivalent).

cooldownOkBuy (bool) : Bool ⏳: Result from applyCooldown for buy.

cooldownOkSell (bool) : Bool ⏳: Result from applyCooldown for sell.

Returns: A tuple containing:

: finalBuySignal (bool) - The final buy signal after all filters.

: finalSellSignal (bool) - The final sell signal after all filters.

@example

= nineLivesUtilLib.applyAllFilters(cooldownBuy, cooldownSell, inDateRange, tradeDirection, volumeOk, tfOk, regimeOk, !drawdownExceeded, cooldownBuy, cooldownSell)

NOTE: This function filters signals generated by your primary entry logic (e.g., EMA crossover).

checkDrawdownExceeded(currentEquity, useMaxDrawdown, maxDrawdownPercent)

Tracks maximum equity and checks if current drawdown exceeds a threshold.

Parameters:

currentEquity (float) : Float: The strategy's current equity (strategy.equity).

useMaxDrawdown (bool) : Bool 📉: Enable max drawdown protection.

maxDrawdownPercent (float) : Float 📉: The maximum allowed drawdown as a percentage.

Returns: True if drawdown protection is enabled and the current drawdown exceeds the threshold, false otherwise.

@example

drawdownExceeded = nineLivesUtilLib.checkDrawdownExceeded(strategy.equity, useMaxDrawdown, maxDrawdownPercent)

if drawdownExceeded

// Consider stopping entries or exiting positions in the strategy script

calculateExitPrice(positionAvgPrice, percentage, isStop, isLong)

Calculates a stop loss or take profit price based on a percentage from the average entry price.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

percentage (float) : Float: The stop loss or take profit percentage (e.g., 2.0 for 2%).

isStop (bool) : Bool: True if calculating a stop loss price, false if calculating a take profit price.

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated stop price or take profit price, or na if no position or percentage is invalid.

@example

longSL = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, stopLossPercent, true, true)

shortTP = nineLivesUtilLib.calculateExitPrice(strategy.position_avg_price, takeProfitPercent, false, false)

calculateTrailingStopLevel(positionAvgPrice, trailOffsetPercent, trailPercent, currentHigh, currentLow, isLong)

Calculates the current trailing stop level for a position.

Parameters:

positionAvgPrice (float) : Float: The average price of the current position (strategy.position_avg_price).

trailOffsetPercent (float) : Float 🔄: The percentage price movement to activate the trailing stop.

trailPercent (float) : Float 🔄: The percentage distance the stop trails behind the price.

currentHigh (float) : Float: The current bar's high (high).

currentLow (float) : Float: The current bar's low (low).

isLong (bool) : Bool: True if the position is long, false if short.

Returns: The calculated trailing stop price if active, otherwise na.

@example

longTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, true)

shortTrailStop = nineLivesUtilLib.calculateTrailingStopLevel(strategy.position_avg_price, trailOffset, trailPercent, high, low, false)

if not na(longTrailStop)

strategy.exit("Long Trail", from_entry="Long", stop=longTrailStop)

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

is_strategyCorrection-Adaptive Trend Strategy (Open-Source)

Core Advantage: Designed specifically for the is_correction indicator, with full transparency and customization options.

Key Features:

Open-Source Code:

✅ Full access to the strategy logic – study how every trade signal is generated.

✅ Freedom to customize – modify entry/exit rules, risk parameters, or add new indicators.

✅ No black boxes – understand and trust every decision the strategy makes.

Built for is_correction:

Filters out false signals during market noise.

Works only in confirmed trends (is_correction = false).

Adaptable for Your Needs:

Change Take Profit/Stop Loss ratios directly in the code.

Add alerts, notifications, or integrate with other tools (e.g., Volume Profile).

For Developers/Traders:

Use the code as a template for your own strategies.

Test modifications risk-free on historical data.

How the Strategy Works:

Main Goal:

Automatically buys when the price starts rising and sells when it starts falling, but only during confirmed trends (ignoring temporary pullbacks).

What You See on the Chart:

📈 Up arrows ▼ (below the candle) = Buy signal.

📉 Down arrows ▲ (above the candle) = Sell signal.

Gray background = Market is in a correction (no trades).

Key Mechanics:

Buy Condition:

Price closes higher than the previous candle + is_correction confirms the main trend (not a pullback).

Example: Red candle → green candle → ▼ arrow → buy.

Sell Condition:

Price closes lower than the previous candle + is_correction confirms the trend (optional: turn off short-selling in settings).

Exit Rules:

Closes trades automatically at:

+0.5% profit (adjustable in settings).

-0.5% loss (adjustable).

Or if a reverse signal appears (e.g., sell signal after a buy).

User-Friendly Settings:

Sell – On (default: ON):

ON → Allows short-selling (selling when price falls).

OFF → Strategy only buys and closes positions.

Revers (default: OFF):

ON → Inverts signals (▼ = sell, ▲ = buy).

%Profit & %Loss:

Adjust these values (0-30%) to increase/decrease profit targets and risk.

Example Scenario:

Buy Signal:

Price rises for 3 days → green ▼ arrow → strategy buys.

Stop loss set 0.5% below entry price.

If price keeps rising → trade closes at +0.5% profit.

Correction Phase:

After a rally, price drops for 1 day → gray background → strategy ignores the drop (no action).

Stop Loss Trigger:

If price drops 0.5% from entry → trade closes automatically.

Key Features:

Correction Filter (is_correction):

Acts as a “noise filter” → avoids trades during temporary pullbacks.

Flexibility:

Disable short-selling, flip signals, or tweak profit/loss levels in seconds.

Transparency:

Open-source code → see exactly how every signal is generated (click “Source” in TradingView).

Tips for Beginners:

Test First:

Run the strategy on historical data (click the “Chart” icon in TradingView).

See how it performed in the past.

Customize It:

Increase %Profit to 2-3% for volatile assets like crypto.

Turn off Sell – On if short-selling confuses you.

Trust the Stop Loss:

Even if you think the price will rebound, the strategy will close at -0.5% to protect your capital.

Where to Find Settings:

Click the strategy name on the top-left of your chart → adjust sliders/toggles in the menu.

Русская Версия

Трендовая стратегия с открытым кодом

Главное преимущество: Полная прозрачность логики и адаптация под ваши нужды.

Особенности:

Открытый исходный код:

✅ Видите всю «кухню» стратегии – как формируются сигналы, когда открываются сделки.

✅ Меняйте правила – корректируйте тейк-профит, стоп-лосс или добавляйте новые условия.

✅ Никаких секретов – вы контролируете каждое правило.

Заточка под is_correction:

Игнорирует ложные сигналы в коррекциях.

Работает только в сильных трендах (is_correction = false).

Гибкая настройка:

Подстройте параметры под свой риск-менеджмент.

Добавьте свои индикаторы или условия для входа.

Для трейдеров и разработчиков:

Используйте код как основу для своих стратегий.

Тестируйте изменения на истории перед реальной торговлей.

Простыми словами:

Почему это удобно:

Открытый код = полный контроль. Вы можете:

Увидеть, как именно стратегия решает купить или продать.

Изменить правила закрытия сделок (например, поставить TP=2% вместо 1.5%).

Добавить новые условия (например, торговать только при высоком объёме).

Примеры кастомизации:

Новички: Меняйте только TP/SL в настройках (без кодинга).

Продвинутые: Добавьте RSI-фильтр, чтобы избегать перекупленности.

Разработчики: Встройте стратегию в свою торговую систему.

Как начать:

Скачайте код из TradingView.

Изучите логику в разделе strategy.entry/exit.

Меняйте параметры в блоке input.* (безопасно!).

Тестируйте изменения и оптимизируйте под свои цели.

Как работает стратегия:

Главная задача:

Автоматически покупает, когда цена начинает расти, и продаёт, когда падает. Но делает это «умно» — только когда рынок в основном тренде, а не во временном откате (коррекции).

Что видно на графике:

📈 Стрелки вверх ▼ (под свечой) — сигнал на покупку.

📉 Стрелки вниз ▲ (над свечой) — сигнал на продажу.

Серый фон — рынок в коррекции (не торгуем).

Как это работает:

Когда покупаем:

Если цена закрылась выше предыдущей и индикатор is_correction показывает «основной тренд» (не коррекция).

Пример: Была красная свеча → стала зелёная → появилась стрелка ▼ → покупаем.

Когда продаём:

Если цена закрылась ниже предыдущей и is_correction подтверждает тренд (опционально, можно отключить в настройках).

Когда закрываем сделку:

Автоматически при достижении:

+0.5% прибыли (можно изменить в настройках).

-0.5% убытка (можно изменить).

Или если появился противоположный сигнал (например, после покупки пришла стрелка продажи).

Настройки для чайников:

«Sell – On» (включено по умолчанию):

Если включено → стратегия будет продавать в шорт.

Если выключено → только покупки и закрытие позиций.

«Revers» (выключено по умолчанию):

Если включить → стратегия будет работать наоборот (стрелки ▼ = продажа, ▲ = покупка).

«%Profit» и «%Loss»:

Меняйте эти цифры (от 0 до 30), чтобы увеличить/уменьшить прибыль и риски.

Пример работы:

Сигнал на покупку:

Цена 3 дня растет → появляется зелёная стрелка ▼ → стратегия покупает.

Стоп-лосс ставится на 0.5% ниже цены входа.

Если цена продолжает расти → сделка закрывается при +0.5% прибыли.

Коррекция:

После роста цена падает на 1 день → фон становится серым → стратегия игнорирует это падение (не закрывает сделку).

Стоп-лосс:

Если цена упала на 0.5% от точки входа → сделка закрывается автоматически.

Важные особенности:

Фильтр коррекций (is_correction):

Это «защита от шума» — стратегия не реагирует на мелкие откаты, работая только в сильных трендах.

Гибкие настройки:

Можно запретить шорты, перевернуть сигналы или изменить уровни прибыли/убытка за 2 клика.

Прозрачность:

Весь код открыт → вы можете увидеть, как формируется каждый сигнал (меню «Исходник» в TradingView).

Советы для новичков:

Начните с теста:

Запустите стратегию на исторических данных (кнопка «Свеча» в окне TradingView).

Посмотрите, как она работала в прошлом.

Настройте под себя:

Увеличьте %Profit до 2-3%, если торгуете валюты.

Отключите «Sell – On», если не понимаете шорты.

Доверяйте стоп-лоссу:

Даже если кажется, что цена развернётся — стратегия закроет сделку при -0.5%, защитив ваш депозит.

Где найти настройки:

Кликните на название стратегии в верхнем левом углу графика → откроется меню с ползунками и переключателями.

Важно: Стратегия предоставляет «рыбу» – чтобы она стала «уловистой», адаптируйте её под свой стиль торговли!

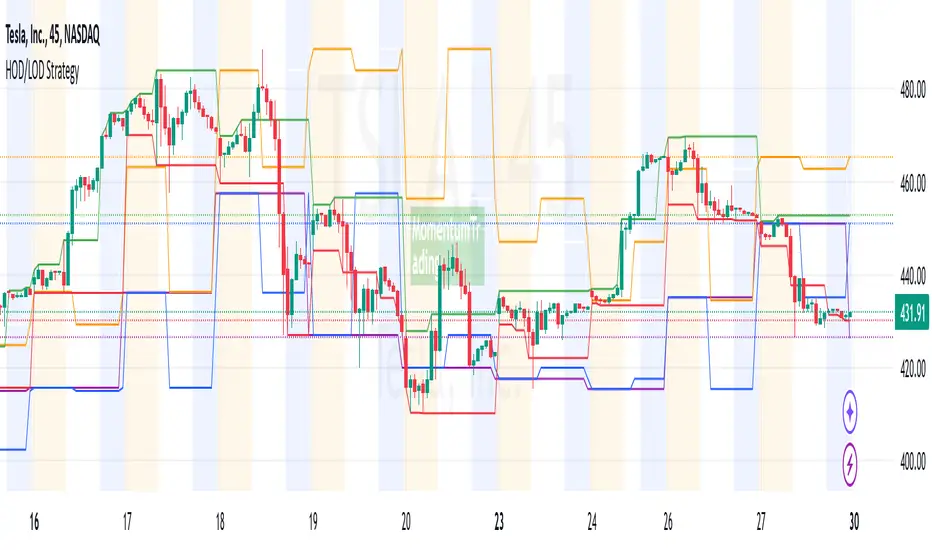

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

Trend Following Strategy with KNN

### 1. Strategy Features

This strategy combines the K-Nearest Neighbors (KNN) algorithm with a trend-following strategy to predict future price movements by analyzing historical price data. Here are the main features of the strategy:

1. **Dynamic Parameter Adjustment**: Uses the KNN algorithm to dynamically adjust parameters of the trend-following strategy, such as moving average length and channel length, to adapt to market changes.

2. **Trend Following**: Captures market trends using moving averages and price channels to generate buy and sell signals.

3. **Multi-Factor Analysis**: Combines the KNN algorithm with moving averages to comprehensively analyze the impact of multiple factors, improving the accuracy of trading signals.

4. **High Adaptability**: Automatically adjusts parameters using the KNN algorithm, allowing the strategy to adapt to different market environments and asset types.

### 2. Simple Introduction to the KNN Algorithm

The K-Nearest Neighbors (KNN) algorithm is a simple and intuitive machine learning algorithm primarily used for classification and regression problems. Here are the basic concepts of the KNN algorithm:

1. **Non-Parametric Model**: KNN is a non-parametric algorithm, meaning it does not make any assumptions about the data distribution. Instead, it directly uses training data for predictions.

2. **Instance-Based Learning**: KNN is an instance-based learning method that uses training data directly for predictions, rather than generating a model through a training process.

3. **Distance Metrics**: The core of the KNN algorithm is calculating the distance between data points. Common distance metrics include Euclidean distance, Manhattan distance, and Minkowski distance.

4. **Neighbor Selection**: For each test data point, the KNN algorithm finds the K nearest neighbors in the training dataset.

5. **Classification and Regression**: In classification problems, KNN determines the class of a test data point through a voting mechanism. In regression problems, KNN predicts the value of a test data point by calculating the average of the K nearest neighbors.

### 3. Applications of the KNN Algorithm in Quantitative Trading Strategies

The KNN algorithm can be applied to various quantitative trading strategies. Here are some common use cases:

1. **Trend-Following Strategies**: KNN can be used to identify market trends, helping traders capture the beginning and end of trends.

2. **Mean Reversion Strategies**: In mean reversion strategies, KNN can be used to identify price deviations from the mean.

3. **Arbitrage Strategies**: In arbitrage strategies, KNN can be used to identify price discrepancies between different markets or assets.

4. **High-Frequency Trading Strategies**: In high-frequency trading strategies, KNN can be used to quickly identify market anomalies, such as price spikes or volume anomalies.

5. **Event-Driven Strategies**: In event-driven strategies, KNN can be used to identify the impact of market events.

6. **Multi-Factor Strategies**: In multi-factor strategies, KNN can be used to comprehensively analyze the impact of multiple factors.

### 4. Final Considerations

1. **Computational Efficiency**: The KNN algorithm may face computational efficiency issues with large datasets, especially in real-time trading. Optimize the code to reduce access to historical data and improve computational efficiency.

2. **Parameter Selection**: The choice of K value significantly affects the performance of the KNN algorithm. Use cross-validation or other methods to select the optimal K value.

3. **Data Standardization**: KNN is sensitive to data standardization and feature selection. Standardize the data to ensure equal weighting of different features.

4. **Noisy Data**: KNN is sensitive to noisy data, which can lead to overfitting. Preprocess the data to remove noise.

5. **Market Environment**: The effectiveness of the KNN algorithm may be influenced by market conditions. Combine it with other technical indicators and fundamental analysis to enhance the robustness of the strategy.

Silver Bullet ICT Strategy [TradingFinder] 10-11 AM NY Time +FVG🔵 Introduction

The ICT Silver Bullet trading strategy is a precise, time-based algorithmic approach that relies on Fair Value Gaps and Liquidity to identify high-probability trade setups. The strategy primarily focuses on the New York AM Session from 10:00 AM to 11:00 AM, leveraging heightened market activity within this critical window to capture short-term trading opportunities.

As an intraday strategy, it is most effective on lower timeframes, with ICT recommending a 15-minute chart or lower. While experienced traders often utilize 1-minute to 5-minute charts, beginners may find the 1-minute timeframe more manageable for applying this strategy.

This approach specifically targets quick trades, designed to take advantage of market movements within tight one-hour windows. By narrowing its focus, the Silver Bullet offers a streamlined and efficient method for traders to capitalize on liquidity shifts and price imbalances with precision.

In the fast-paced world of forex trading, the ability to identify market manipulation and false price movements is crucial for traders aiming to stay ahead of the curve. The Silver Bullet Indicator simplifies this process by integrating ICT principles such as liquidity traps, Order Blocks, and Fair Value Gaps (FVG).

These concepts form the foundation of a tool designed to mimic the strategies of institutional players, empowering traders to align their trades with the "smart money." By transforming complex market dynamics into actionable insights, the Silver Bullet Indicator provides a powerful framework for short-term trading success

Silver Bullet Bullish Setup :

Silver Bullet Bearish Setup :

🔵 How to Use

The Silver Bullet Indicator is a specialized tool that operates within the critical time windows of 9:00-10:00 and 10:00-11:00 in the forex market. Its design incorporates key principles from ICT (Inner Circle Trader) methodology, focusing on concepts such as liquidity traps, CISD Levels, Order Blocks, and Fair Value Gaps (FVG) to provide precise and actionable trade setups.

🟣 Bullish Setup

In a bullish setup, the indicator starts by marking the high and low of the session, serving as critical reference points for liquidity. A typical sequence involves a liquidity grab below the low, where the price manipulates retail traders into selling positions by breaching a key support level.

This movement is often orchestrated by smart money to accumulate buy orders. Following this liquidity grab, a market structure shift (MSS) occurs, signaled by the price breaking the CISD Level—a confirmation of bullish intent. The indicator then highlights an Order Block near the CISD Level, representing the zone where institutional buying is concentrated.

Additionally, it identifies a Fair Value Gap, which acts as a high-probability area for price retracement and trade entry. Traders can confidently take long positions when the price revisits these zones, targeting the next significant liquidity pool or resistance level.

Bullish Setup in CAPITALCOM:US100 :

🟣 Bearish Setup

Conversely, in a bearish setup, the price manipulates liquidity by creating a false breakout above the high of the session. This move entices retail traders into long positions, allowing institutional players to enter sell orders.

Once the price reverses direction and breaches the CISD Level to the downside, a change of character (CHOCH) becomes evident, confirming a bearish market structure. The indicator highlights an Order Block near this level, indicating the origin of the institutional sell orders, along with an associated FVG, which represents an imbalance zone likely to be revisited before the price continues downward.

By entering short positions when the price retraces to these levels, traders align their strategies with the anticipated continuation of bearish momentum, targeting nearby liquidity voids or support zones.

Bearish Setup in OANDA:XAUUSD :

🔵 Settings

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The Silver Bullet Indicator is a cutting-edge tool designed specifically for forex traders who aim to leverage market dynamics during critical liquidity windows. By focusing on the highly active 9:00-10:00 and 10:00-11:00 timeframes, the indicator simplifies complex market concepts such as liquidity traps, Order Blocks, Fair Value Gaps (FVG), and CISD Levels, transforming them into actionable insights.

What sets the Silver Bullet Indicator apart is its precision in detecting false breakouts and market structure shifts (MSS), enabling traders to align their strategies with institutional activity. The visual clarity of its signals, including color-coded zones and directional arrows, ensures that both novice and experienced traders can easily interpret and apply its findings in real-time.

By integrating ICT principles, the indicator empowers traders to identify high-probability entry and exit points, minimize risk, and optimize trade execution. Whether you are capturing short-term price movements or navigating complex market conditions, the Silver Bullet Indicator offers a robust framework to enhance your trading performance.

Ultimately, this tool is more than just an indicator; it is a strategic ally for traders who seek to decode the movements of smart money and capitalize on institutional strategies. With the Silver Bullet Indicator, traders can approach the market with greater confidence, precision, and profitability.

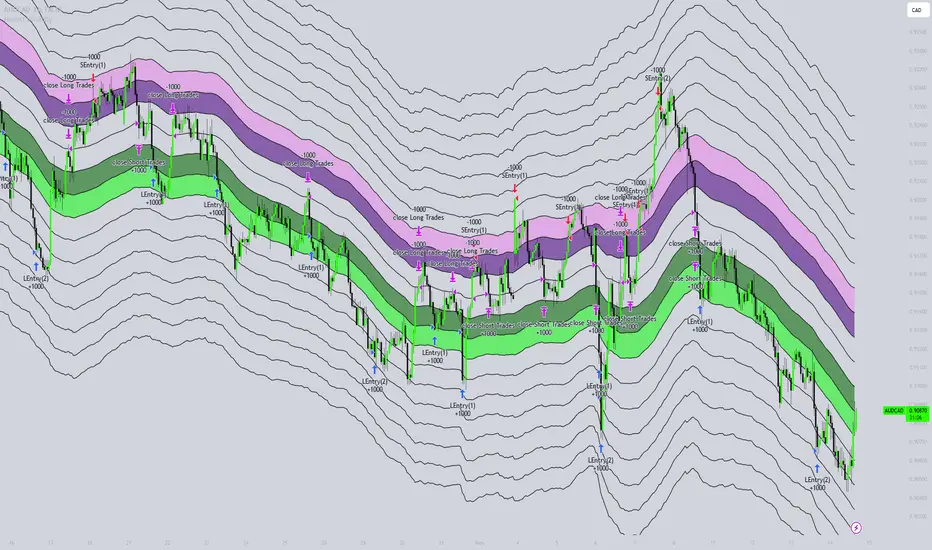

Honest Volatility Grid [Honestcowboy]The Honest Volatility Grid is an attempt at creating a robust grid trading strategy but without standard levels.

Normal grid systems use price levels like 1.01;1.02;1.03;1.04... and place an order at each of these levels. In this program instead we create a grid using keltner channels using a long term moving average.

🟦 IS THIS EVEN USEFUL?

The idea is to have a more fluid style of trading where levels expand and follow price and do not stick to precreated levels. This however also makes each closed trade different instead of using fixed take profit levels. In this strategy a take profit level can even be a loss. It is useful as a strategy because it works in a different way than most strategies, making it a good tool to diversify a portfolio of trading strategies.

🟦 STRATEGY

There are 10 levels below the moving average and 10 above the moving average. For each side of the moving average the strategy uses 1 to 3 orders maximum (3 shorts at top, 3 longs at bottom). For instance you buy at level 2 below moving average and you increase position size when level 6 is reached (a cheaper price) in order to spread risks.

By default the strategy exits all trades when the moving average is reached, this makes it a mean reversion strategy. It is specifically designed for the forex market as these in my experience exhibit a lot of ranging behaviour on all the timeframes below daily.

There is also a stop loss at the outer band by default, in case price moves too far from the mean.

What are the risks?

In case price decides to stay below the moving average and never reaches the outer band one trade can create a very substantial loss, as the bands will keep following price and are not at a fixed level.

Explanation of default parameters

By default the strategy uses a starting capital of 25000$, this is realistic for retail traders.

Lot sizes at each level are set to minimum lot size 0.01, there is no reason for the default to be risky, if you want to risk more or increase equity curve increase the number at your own risk.

Slippage set to 20 points: that's a normal 2 pip slippage you will find on brokers.

Fill limit assumtion 20 points: so it takes 2 pips to confirm a fill, normal forex spread.

Commission is set to 0.00005 per contract: this means that for each contract traded there is a 5$ or whatever base currency pair has as commission. The number is set to 0.00005 because pinescript does not know that 1 contract is 100000 units. So we divide the number by 100000 to get a realistic commission.

The script will also multiply lot size by 100000 because pinescript does not know that lots are 100000 units in forex.

Extra safety limit

Normally the script uses strategy.exit() to exit trades at TP or SL. But because these are created 1 bar after a limit or stop order is filled in pinescript. There are strategy.orders set at the outer boundaries of the script to hedge against that risk. These get deleted bar after the first order is filled. Purely to counteract news bars or huge spikes in price messing up backtest.

🟦 VISUAL GOODIES

I've added a market profile feature to the edge of the grid. This so you can see in which grid zone market has been the most over X bars in the past. Some traders may wish to only turn on the strategy whenever the market profile displays specific characteristics (ranging market for instance).

These simply count how many times a high, low, or close price has been in each zone for X bars in the past. it's these purple boxes at the right side of the chart.

🟦 Script can be fully automated to MT5

There are risk settings in lot sizes or % for alerts and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

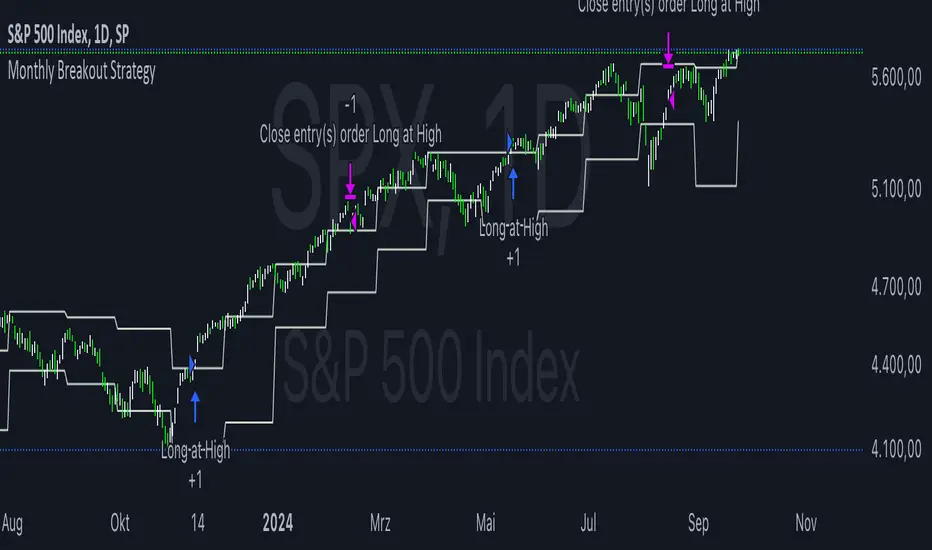

Monthly Breakout StrategyThis Monthly High/Low Breakout Strategy is designed to take long or short positions based on breakouts from the high or low of the previous month. Users can select whether they want to go long at a breakout above the previous month’s high, short at a breakdown below the previous month’s low, or use the reverse logic. Additionally, it includes a month filter, allowing trades to be executed only during user-specified months.

Breakout strategies, particularly those based on monthly highs and lows, aim to capitalize on price momentum. These systems rely on the assumption that once a significant price level is breached (such as the previous month's high or low), the market is likely to continue moving in the same direction due to increased volatility and trend-following behaviors by traders. Studies have demonstrated the potential effectiveness of breakout strategies in financial markets.

Scientific Evidence Supporting Breakout Strategies:

Momentum in Financial Markets:

Research on momentum-based strategies, which include breakout trading, shows that securities breaking key levels of support or resistance tend to continue their price movement in the direction of the breakout. Jegadeesh and Titman (1993) found that stocks with strong performance over a given period tend to continue performing well in subsequent periods, a principle also applied to breakout strategies.

Behavioral Finance:

The psychological factor of herd behavior is one of the driving forces behind breakout strategies. When prices break out of a key level (such as a monthly high), it triggers increased buying or selling pressure as traders join the trend. Barberis, Shleifer, and Vishny (1998) explained how cognitive biases, such as overconfidence and sentiment, can amplify price trends, which breakout strategies attempt to exploit.

Market Efficiency:

While markets are generally efficient, periods of inefficiency can occur, particularly around the breakouts of significant price levels. These inefficiencies often result in temporary price trends, which breakout strategies can exploit before the market corrects itself (Fama, 1970).

Risk Considerations:

Despite the potential for profit, the Monthly Breakout Strategy comes with several risks:

False Breakouts:

One of the most common risks in breakout strategies is the occurrence of false breakouts. These happen when the price temporarily moves above (or below) a key level but quickly reverses direction, causing losses for traders who entered positions too early. This is particularly risky in low-volatility environments.

Market Volatility:

Monthly breakout strategies rely on momentum, which may not be consistent across different market conditions. During periods of low volatility, price breakouts might lack the follow-through required for the strategy to succeed, leading to poor performance.

Whipsaw Risk:

The strategy is vulnerable to whipsaw markets, where prices oscillate around key levels without establishing a clear direction. This can result in frequent entry and exit signals that lead to losses, especially if trading costs are not managed properly.

Overfitting to Past Data:

If the month-selection filter is overly optimized based on historical data, the strategy may suffer from overfitting—performing well in backtests but poorly in real-time trading. This happens when strategies are tailored to past market conditions that may not repeat.

Conclusion:

While monthly breakout strategies can be effective in markets with strong momentum, they are subject to several risks, including false breakouts, volatility dependency, and whipsaw behavior. It is crucial to backtest this strategy thoroughly and ensure it aligns with your risk tolerance before implementing it in live trading.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Barberis, N., Shleifer, A., & Vishny, R. (1998). A Model of Investor Sentiment. Journal of Financial Economics, 49(3), 307-343.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Larry Connors RSI 3 StrategyThe Larry Connors RSI 3 Strategy is a short-term mean-reversion trading strategy. It combines a moving average filter and a modified version of the Relative Strength Index (RSI) to identify potential buying opportunities in an uptrend. The strategy assumes that a short-term pullback within a long-term uptrend is an opportunity to buy at a discount before the trend resumes.

Components of the Strategy:

200-Day Simple Moving Average (SMA): The price must be above the 200-day SMA, indicating a long-term uptrend.

2-Period RSI: This is a very short-term RSI, used to measure the speed and magnitude of recent price changes. The standard RSI is typically calculated over 14 periods, but Connors uses just 2 periods to capture extreme overbought and oversold conditions.

Three-Day RSI Drop: The RSI must decline for three consecutive days, with the first drop occurring from an RSI reading above 60.

RSI Below 10: After the three-day drop, the RSI must reach a level below 10, indicating a highly oversold condition.

Buy Condition: All the above conditions must be satisfied to trigger a buy order.

Sell Condition: The strategy closes the position when the RSI rises above 70, signaling that the asset is overbought.

Who Was Larry Connors?

Larry Connors is a trader, author, and founder of Connors Research, a firm specializing in quantitative trading research. He is best known for developing strategies that focus on short-term market movements. Connors co-authored several popular books, including "Street Smarts: High Probability Short-Term Trading Strategies" with Linda Raschke, which has become a staple among traders seeking reliable, rule-based strategies. His research often emphasizes simplicity and robust testing, which appeals to both retail and institutional traders.

Scientific Foundations

The Relative Strength Index (RSI), originally developed by J. Welles Wilder in 1978, is a momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100 and is typically used to identify overbought or oversold conditions in an asset. However, the use of a 2-period RSI in Connors' strategy is unconventional, as most traders rely on longer periods, such as 14. Connors' research showed that using a shorter period like 2 can better capture short-term reversals, particularly when combined with a longer-term trend filter such as the 200-day SMA.

Connors' strategies, including this one, are built on empirical research using historical data. For example, in a study of over 1,000 signals generated by this strategy, Connors found that it performed consistently well across various markets, especially when trading ETFs and large-cap stocks (Connors & Alvarez, 2009).

Risks and Considerations

While the Larry Connors RSI 3 Strategy is backed by empirical research, it is not without risks:

Mean-Reversion Assumption: The strategy is based on the premise that markets revert to the mean. However, in strong trending markets, the strategy may underperform as prices can remain oversold or overbought for extended periods.

Short-Term Nature: The strategy focuses on very short-term movements, which can result in frequent trading. High trading frequency can lead to increased transaction costs, which may erode profits.

Market Conditions: The strategy performs best in certain market environments, particularly in stable uptrends. In highly volatile or strongly trending markets, the strategy's performance can deteriorate.

Data and Backtesting Limitations: While backtests may show positive results, they rely on historical data and do not account for future market conditions, slippage, or liquidity issues.

Scientific literature suggests that while technical analysis strategies like this can be effective in certain market conditions, they are not foolproof. According to Lo et al. (2000), technical strategies may show patterns that are statistically significant, but these patterns often diminish once they are widely adopted by traders.

References

Connors, L., & Alvarez, C. (2009). Short-Term Trading Strategies That Work. TradingMarkets Publishing Group.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation. The Journal of Finance, 55(4), 1705-1770.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research

Monthly Purchase Strategy with Dynamic Contract Size This trading strategy is designed to automate monthly purchases of a security, adjusting the size of each purchase based on the percentage of the portfolio's equity. The key features of this strategy include:

Monthly Purchases: The strategy buys the security on a specified day of each month, based on the user's input.

Dynamic Position Sizing: The size of each purchase is calculated as a percentage of the current equity. This allows the position size to adjust dynamically with the portfolio's performance.

Slippage and Commission Considerations: Slippage is simulated by adjusting the entry price by a set number of ticks, while commissions are factored in as fixed costs per trade.

Drawdown Calculation: The strategy tracks the highest equity value and calculates the drawdown, which is the percentage decrease from this peak equity. This helps in assessing the performance and risk of the strategy.

Benefits of the Strategy

Automated Investment: The strategy automates the investment process, reducing the need for manual trading decisions and ensuring consistent execution.

Dynamic Position Sizing: By adjusting the purchase size based on the portfolio’s equity, the strategy helps in managing risk and capitalizing on market movements proportionally to the portfolio’s performance.

Regular Investments: Investing on a regular schedule helps in averaging the purchase price of the security, which can reduce the impact of short-term volatility.

Risk Management: Monitoring drawdown helps in assessing the risk and performance of the strategy, providing insights into potential losses relative to the highest equity value.

Scientific Documentation on ETF Savings Plans

1. Dollar-Cost Averaging and Investment Behavior:

Title: "The Benefits of Dollar-Cost Averaging: A Study of Investment Behavior"

Authors: William F. Sharpe

Journal: Financial Analysts Journal, 1994

Summary: This study discusses the concept of dollar-cost averaging (DCA), which involves investing a fixed amount of money at regular intervals regardless of market conditions. The study highlights that DCA can reduce the impact of market volatility and lower the average cost of investments over time.

Reference: Sharpe, W. F. (1994). The Benefits of Dollar-Cost Averaging: A Study of Investment Behavior. Financial Analysts Journal, 50(4), 27-36.

2. ETFs and Long-Term Investment Strategies:

Title: "Exchange-Traded Funds and Their Role in Long-Term Investment Strategies"

Authors: John C. Bogle

Journal: The Journal of Portfolio Management, 2007

Summary: This paper explores the advantages of using ETFs for long-term investment strategies, emphasizing their low costs, tax efficiency, and diversification benefits. It also discusses how ETFs can be used effectively in automated investment plans like ETF savings plans.

Reference: Bogle, J. C. (2007). Exchange-Traded Funds and Their Role in Long-Term Investment Strategies. The Journal of Portfolio Management, 33(4), 14-25.

3. Risk and Return in ETF Investments:

Title: "Risk and Return Characteristics of Exchange-Traded Funds"

Authors: Eugene F. Fama and Kenneth R. French

Journal: Journal of Financial Economics, 2010

Summary: Fama and French analyze the risk and return characteristics of ETFs compared to traditional mutual funds. The study provides insights into how ETFs can be a viable option for investors seeking diversified exposure while managing risk and optimizing returns.

Reference: Fama, E. F., & French, K. R. (2010). Risk and Return Characteristics of Exchange-Traded Funds. Journal of Financial Economics, 96(2), 257-278.

4. The Impact of Automated Investment Plans:

Title: "The Impact of Automated Investment Plans on Portfolio Performance"

Authors: David G. Blanchflower and Andrew J. Oswald